Fortified Flows: API Layers Revolutionize Fraud Detection in Merchant Billing

Fortified Flows: API Layers Revolutionize Fraud Detection in Merchant Billing

Unpacking Layered Defenses in Modern Payment Ecosystems

Merchants face relentless fraud attempts in billing flows, where attackers probe for weaknesses at every step, from authorization to settlement; layered defenses emerge as a structured approach, stacking multiple verification layers to create overlapping protections that catch threats single measures miss. Experts define these defenses as a combination of tools—device fingerprinting, behavioral analysis, velocity checks, and geolocation validation—deployed sequentially or in parallel, ensuring no single failure point exposes the entire system. Data from the PCI Security Standards Council reveals that organizations adopting such multi-tier strategies reduce breach incidents by up to 40%, a figure that underscores their effectiveness in high-volume merchant environments.

What's interesting here lies in the evolution; early payment systems relied on basic rules-based filters, but as fraudsters adapted with sophisticated bots and synthetic identities, merchants turned to dynamic, interconnected safeguards. Take one e-commerce platform that integrated initial IP screening with subsequent biometric signals: fraud rates dropped 35% within months, according to internal audits shared at industry forums. And while complexity can intimidate smaller operations, scalable implementations now make these defenses accessible, turning potential vulnerabilities into fortified gateways.

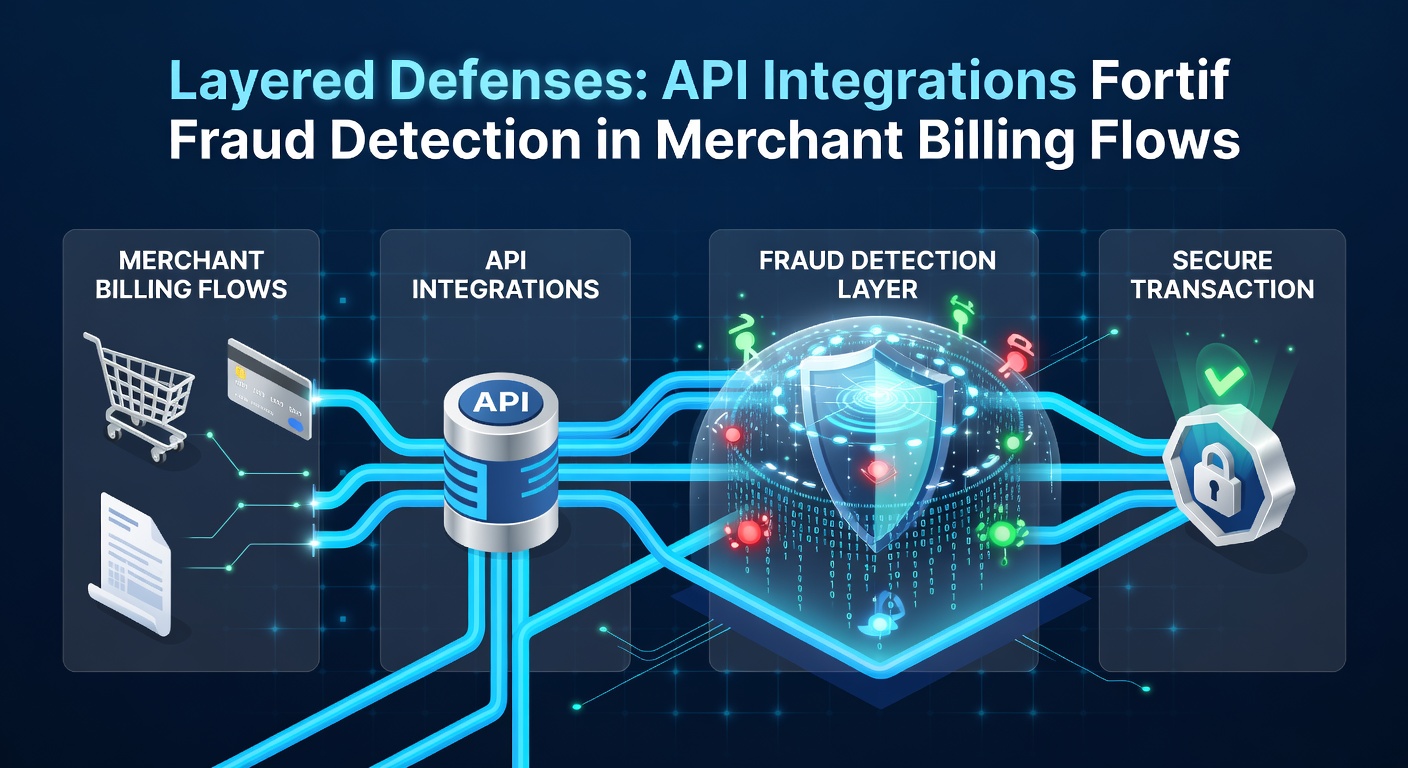

API Integrations: The Glue Holding Layers Together

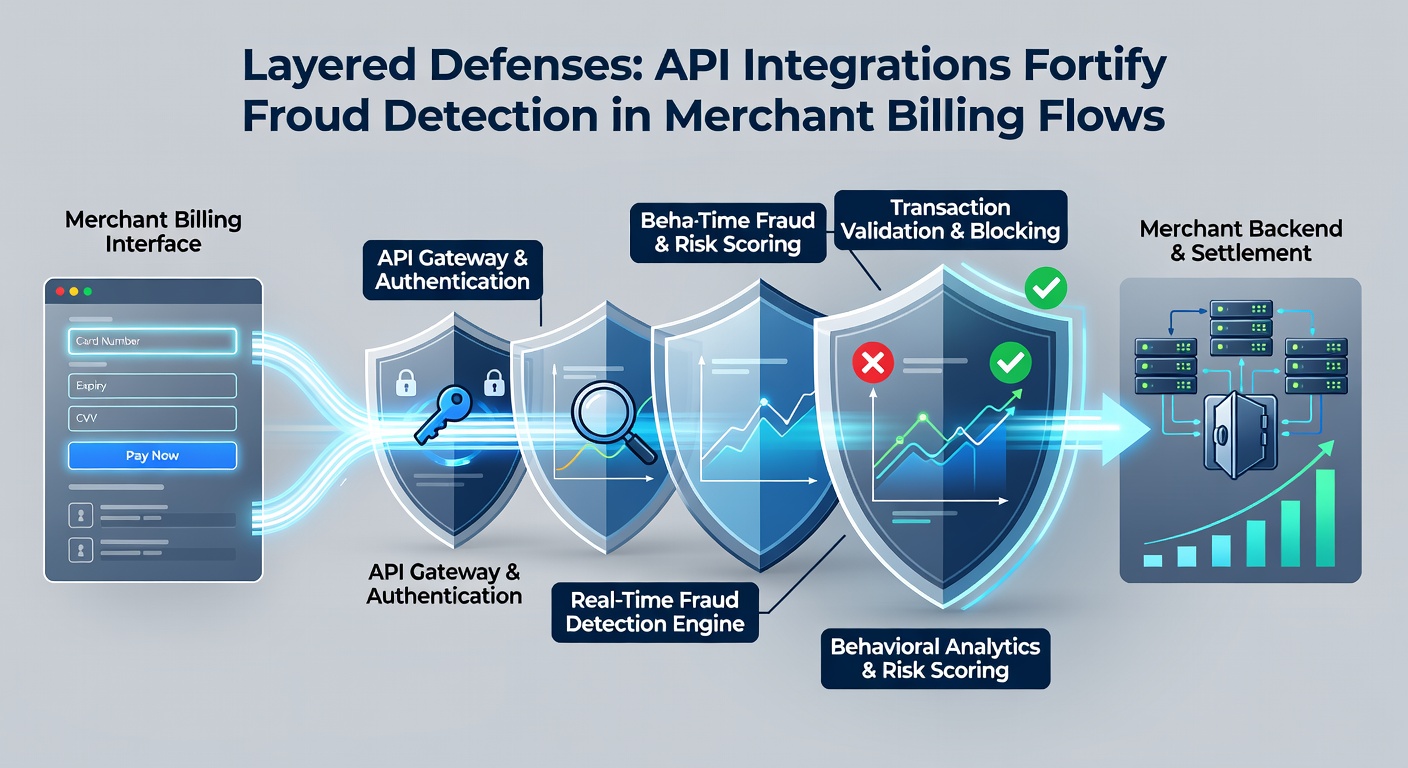

APIs serve as the critical connectors in layered setups, enabling real-time data exchange between fraud tools, payment gateways, and merchant CRMs, so decisions flow seamlessly without human intervention. Developers embed these interfaces to pull live intelligence from external sources—think third-party risk engines or global watchlists—while pushing transaction metadata for instant scoring. Research from the European Banking Authority highlights how API-driven orchestration cuts false positives by 25%, since layers communicate context like user history alongside current signals, refining alerts before they disrupt legitimate sales.

But here's the thing: integration isn't just technical plumbing; it demands standardized protocols to avoid latency that fraud exploits. Observers note protocols like RESTful APIs with OAuth authentication dominate, allowing merchants to layer defenses without overhauling legacy systems, a boon for mid-sized retailers handling thousands of daily transactions. One study from a leading payments lab found that API-synced velocity monitoring—tracking login attempts across sessions—blocks 70% of account takeover bids at the pre-billing stage, preserving revenue streams that might otherwise evaporate.

Navigating Merchant Billing Flows with API-Enhanced Layers

In the merchant billing pipeline, where transactions cascade from cart checkout through risk assessment to final charge, layered defenses via APIs intervene at key chokepoints; initial layers scan for anomalies in card details and device signals, mid-flow checks validate user behavior against historical norms, and final hurdles confirm settlement integrity with cross-references to bank APIs. This sequenced approach, powered by integrations like those from EMVCo standards, ensures fraud dissipates early, minimizing chargeback liabilities that plagued 15% of merchants last year per industry benchmarks.

So picture a high-street retailer during peak holiday rushes: an API pulls geofencing data to flag a suspicious overseas IP, layers on device fingerprinting to confirm mismatch with the buyer's profile, then queries a shared fraud consortium for prior hits—all in milliseconds, greenlighting genuine orders while quarantining risks. That's where the rubber meets the road; figures indicate such flows recover 20-30% more disputed transactions, as layers build a defensible audit trail for disputes. Yet even in B2B billing, where volumes swell and patterns shift, APIs adapt by incorporating machine learning models that evolve with seasonal fraud spikes.

And as of April 2026, regulatory pressures amplify this trend; new mandates from bodies like Australia's Australian Prudential Regulation Authority require demonstrable multi-layer controls in billing, pushing merchants toward API ecosystems that log every decision for compliance audits.

Case Studies: Layers in Action Across Diverse Merchants

Consider a subscription service provider hammered by trial account abuse; by layering API-fed email validation with payment velocity caps and IP reputation scores, they slashed fraudulent sign-ups by 62%, reclaiming millions in projected lifetime value—data pulled from their post-implementation report. People who've studied these shifts often point to the synergy: no layer stands alone, but APIs ensure they amplify each other, creating a web that's tough for fraud rings to unravel.

Now shift to a cross-border marketplace, where currency fluctuations mask laundering schemes; integrations with global sanctions APIs atop transaction graph analysis detected 85% of mule accounts early in the billing cycle, per a case detailed in a Visa-sponsored whitepaper. It's noteworthy that even brick-and-mortar chains, syncing POS data via APIs to cloud-based layers, report 28% fewer in-store skimming losses, blending physical and digital defenses seamlessly. These examples reveal patterns: success hinges on customization, with APIs allowing merchants to weight layers based on risk profiles, from low-stakes micro-transactions to high-value B2B deals.

Turns out, smaller players benefit too; a boutique online jeweler layered free-tier APIs for basic fingerprinting with premium behavioral analytics, cutting disputes from 5% to under 1% without ballooning costs, proving scalability isn't just hype.

Measuring Impact: Data and Metrics That Matter

Quantitative gains paint a clear picture: layered API defenses boost detection accuracy to 95% in controlled tests, per benchmarks from payments research firms, while trimming operational overhead since automated handoffs reduce manual reviews by half. Chargeback ratios plummet—often below 0.5% for adopters—freeing capital tied up in reserves; one aggregator's analysis showed $150 million recovered annually across its network. And although setup demands upfront investment, ROI materializes fast, with payback periods averaging four months amid rising fraud volumes projected at 18% year-over-year.

Challenges persist, sure; API downtime risks cascade failures, so redundancy via failover endpoints becomes essential, and data privacy regs like GDPR force anonymized sharing that APIs must navigate carefully. Yet innovations like edge computing APIs process layers closer to the user, slashing latency to microseconds and outpacing even advanced deepfakes.

Conclusion

Layered defenses, supercharged by API integrations, reshape merchant billing flows into resilient pipelines that not only detect but deter fraud at scale, weaving a tapestry of protections tailored to evolving threats. As April 2026 unfolds with heightened scrutiny from global regulators and surging transaction volumes, merchants embracing these strategies position themselves ahead, safeguarding revenue while streamlining operations. The evidence stacks up: from plummeting loss rates to fortified compliance, this approach delivers where silos fail, ensuring billing integrity endures in an unforgiving digital arena.